A Review of Markets 2022

2023 Outlook: Sandwiches for the road:

2022 was the worst year for the stock market since 2008. The S&P 500 and the NASDAQ were down in the range of -19% and -33%, respectively. However, KAMSouth had a very successful year in 2022, as we easily outperformed the major benchmark indexes. Higher interest rates and valuation compression in technology stocks drove the large negative returns for these two indexes.

Tesla’s stock is a representation of what took place in terms of the bubble in the technology sector. Tesla shares have lost 63%, from a peak market value of $1.24 trillion to $389 billion. At current price levels, one could purchase twelve Ford’s (the entire business) for one Tesla.

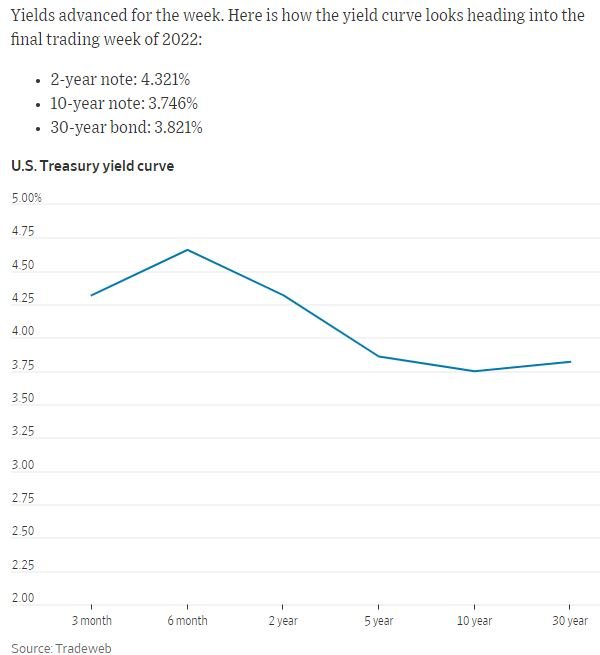

The shape of the yield curve is telling us a story:

The Treasury yield curve is published weekly in the FRED database (St. Louis Federal Reserve Bank). A normal shaping treasury yield curve is upward-sloping, with the rate on longer-term bonds carrying higher interest rates than shorter-term bonds. Today, we have the exact opposite! We have a downward-sloping yield curve which is referred to as an inverted yield curve. This is a rare phenomenon.

An inverted yield curve suggests that the bond market believes we are heading into an economic recession in 2023. Currently, the 2-year note was 4.3% versus the 10-year note of 3.7% and 30-year Bond of 3.8%. The graph is today’s inverted yield curve where short-term rates are higher than long-term rates. Interest rates are the key variable to watch to understand, where the economy is going.

Unemployment Rate:

The current economic environment of low unemployment of 3.5% and high inflation of 7.1% paints a problematic outlook. Inflationary pressures still abound in the real economy. For example, Delta pilots received a 34% wage increase in December. This type of labor inflation will be tough to eliminate. Going forward, the unemployment rate will need to rise to the 5%-6% level to provide a path to lower inflation.

We can not start a new economic up-cycle with 3.5% unemployment. The Fed has its work cut out for it in 2023. Finally, high debt levels in the U.S. could become a crisis issue. Today, debt is 150% of domestic output. Rising interest rates only work when fiscal policy comes behind and sharply lowers spending. This is not happening as the House approved another $1.7 Trillion Omnibus spending bill on December 23, 2022.

Portfolio Positioning for 2023:

We exited 2022 with a significant cash position. Our success was due to our stock selection in Energy and Banking. Our portfolio looks very different from the market benchmarks due to our focus on low-valuation stocks that trade at a price below intrinsic value. These characteristics can be financial resources, factories, brand names, growth potential, bank branches in unique growing areas, and the ability to generate earnings and dividends. For example, one investment on our radar is trading at 0.55 price-to-tangible book value with a 4.6% dividend yield and around 2,000 branches. As Warren Buffett would say, “we are buying fifty-cent dollars.” We continue to be bullish on the energy sector. Lack of capital spending over the last decade has provided a supply constrained environment where oil company profits are in an upward cycle. The global uncertainty with Russia, Ukraine, and China adds to our positive view that oil demand and traditional natural resource companies are uniquely positioned to capitalize on higher earnings power. In our experience, trends in motion tend to stay in motion longer than expected. Finally, fixed income (corporate bonds) with a yield to maturity in the range of 5%-6% look attractive for their income characteristics.

Food For Thought:

Early in my investment career, I came across a poster of a grizzly bear with the punchline, “This is a Bear and Most Mutual Fund Managers Have Never Seen One.”

I think the statement rings true today! Most mutual fund managers are young kids that fell in love with cryptocurrency, bitcoin and, FTX. We avoided the entire experience because we would not put our client’s precious hard-earned money into an investment that had unquantifiable risk.

We have no particular bias when it comes to choosing investments. We search for the highest after-tax returns that have a margin of safety. Unfortunately, the failure of investors to heed this simple framework was seen last year. For 2023, we are in a solid position to execute our investment strategy. The days of passive-index investing appear to be over. Currently, a wide valuation disparity provides attractive opportunities for active, value-oriented, bottom-up investment managers like KAMSouth.

Warmest regards,

Dr. Christian Koch, CFP®, CPWA®, CDFA®, RICP®