We Love Bonds

The market has been experiencing another correction period due to the concerns over the Israel-Hamas war. Year to date, we have seen a lack of breath in the S&P 500 as 493 companies (excluding the magnificent 7-tech stocks) have had flat return performances.

In my opinion, the character of the market feels different. Investors are having to digest the uncertainty and probability of war, higher interest rates for longer, a dysfunctional Washington, much higher inflation, and too much fiscal spending. This has led to large U.S. budget deficits. All of these factors are negative forces putting pressure on stocks.

I bring these facts to your attention because it appears we have reached an inflection point where equities (stocks) could be under pressure for a more extended period. In times of low visibility and high uncertainty, the P/E multiple of the market usually declines, even if we have rising earnings.

October 19, 2023, the WSJ had an article discussing the time-honored Wall Street trusted 60-40 investment strategy. This type of portfolio had its worst performance in generations last year due to higher interest rates and inflation. This is a mix of 60% bonds and 40% stocks.

As we advance, a prolonged period of higher rates and higher inflation will pressure both stocks and bonds (more on stocks). This capital market environment looks much different than we have seen over the last 15 years.

We Love Bonds:

The next phase of successful investment will be using the 1970s-1980s (President Carter years) playbook of Yield investing, which focuses on higher yield as the main component of return for retirement portfolios. Going forward, we will be looking to make new investments in corporate bonds and preferred stock of companies that have a high coupon yield and consistent cash flow to pay the interest and principal.

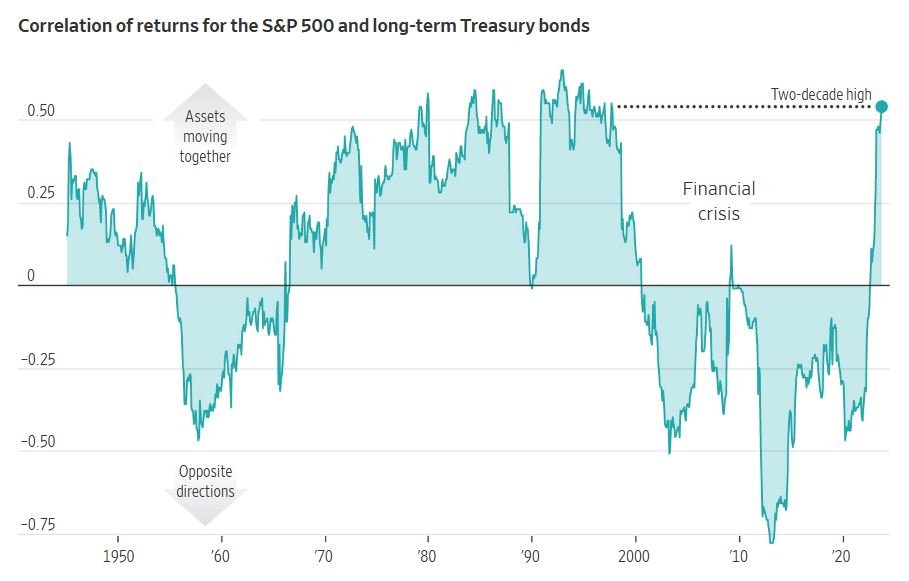

There are two reasons to make this change: 1) We are trying to lower the total risk in our portfolio to get the odds on our side if we experience more market disruptions; 2) It is essential to know where we stand in the market cycle. It is our belief that we are long in the cycle, and it’s essential to pay attention to changes in the investment environment. High inflation and higher rates have changed the character, and thus the odds (risk) have changed. As you can see from the Graph (above), Preferred stock and Bonds (debt) have a lower risk profile to the investor than common stock. As of this writing, the 10-year t-bond yields 4.91% on risk-free money. This means by taking on no risk, the investor can earn a return in the range of 5%.

Back to Basics:

The primary finance concept of Interest on Interest is essential to consider. The recent higher level of bond yields and the uncertainty of geopolitical risk in the Middle East emphasize the importance of interest-on-interest and how fixed income and preferred stock securities will play an essential role in a retirement portfolio. Compound interest at high rates will start to be one of the most potent growth forces in the next few years.

Dr. Danielsen states in his textbook, Foundations of Financial Management 18th Edition, “the corporate bond represents the basic long-term debt instrument for most large U.S. corporations. The bond agreement specifies such basic items as the par value, the coupon rate, and the maturity date.” As further context, the Coupon Rate is the actual interest rate on the bond, usually payable in semiannual installments. Currently, we are finding Bonds and Preferred Stocks very attractive relative to stocks given the lower visibility and uncertain backdrop we find ourselves in.

For example, Citigroup has a fixed-rate preferred stock with a coupon of 7.625% for a term of 5 years. This preferred stock security has a par value of $1,000 and can be purchased below par value of around $96, which gives it a yield to maturity (YTM) above 8%. This is 300 basis points above the risk-free rate.

Commercial Banks: Update

As we advance, it is difficult to be categorical about the exposure of banks domestically to a U.S. recession, should one develop in the next 12 months. In general, we consider banks better prepared for the next downturn than they were for the previous one, as credit cultures have been strengthened. However, monetary policy has been in restrictive mode for an extended period and has become tighter with the recent dramatic back-up in rates.

During the latest Q2 2023 earnings calls we have listened to, it appears some banks are struggling with four main issues: 1) funding pressure-cost of funds is rising; 2) Holding of bonds that have paper losses; 3) higher rate environment has slowed loan growth; 4) One-off credit quality issues.

Banking is neither a primary global industry (like energy, pharmaceuticals, or semiconductors) nor a purely regional one that can operate apart from U.S. economic trends. Going forward, we may reduce exposure to banks in portfolios on a name-by-name basis and with a high degree of urgency if a U.S. Recession becomes a reality. However, we will hold on to a few core franchises where we feel their footprint and deposit base are attractive to another more prominent player who would purchase stock at a premium to book value.

The New Oil Wars:

Going forward, we believe dirty oil (petroleum) will be the next place to invest and put capital to work. Currently, the U.S. only has 17 days of oil in the Strategic Petroleum Reserve (SPR). Just like we have seen an end to zero interest rates, it appears we have seen an end to cheap oil.

This means domestic and international energy stocks should continue to have higher earnings power based on higher realized price returns on WTI. Over the last two years, U.S. energy policy has reduced supply, which will only add to a global supply crunch and a future price shock like we saw in 1973. Panic could set the stage for over $100 WTI if the U.S. is forced into a war in the Middle East. Today, we face a world crisis of vast dimensions made by the reality that every nation still needs oil to live and survive. Any significant interruption stemming from political decisions, political instability, terrorist actions, or major panic would entail severe disruptions and higher prices. We are bullish on petroleum & oil service stocks. Currently trading at a forward P/E multiple of 6.6x, Devon Energy (DVN) has an attractive reward-to-risk ratio.

Investment Strategy:

Going forward, we intend to make a few minor adjustments to the portfolio, moving more dollars into cash, fixed income, and preferred stock securities and lowering our exposure to equities (stocks).

The bible for value investing, Security Analysis, is a textbook that has been around for 90 years and discusses the theory and practice of investing. This year, McGraw Hill published an updated 7th edition of the textbook with a foreword by Warren Buffett and Seth Klarman. As I re-read this text, the timeless wisdom inspired me to navigate the uncertain economic, geopolitical, and capital market environment. It states, “The world of investments is one of unlimited choices, significant opportunity, great rewards, shifting landscapes, untold nuances, and serious perils. Against that backdrop, investors must weigh multiple and sometimes competing objectives: generating income, growing principal over time, protecting against loss and the ravages of inflation, and maintaining a degree of liquidity to provide future flexibility and meet unexpected needs. Finding the right balance is essential.”

As always, please be in touch if you would like to discuss further details.

Dr. Christian Koch, CFP®, CPWA®, CDFA®, RICP®