Warren Buffett's Interpretation of Financial Statements: A Unique Classroom Learning Experience

Zack Kifer was a student of Dr. Koch in his Investments class (BUS 422) at NC State University. He is graduating with a degree in finance. His LinkedIn profile: https://www.linkedin.com/in/zach-kifer/

The Kraft Heinz Company

Zach Kifer

A company with a durable competitive advantage is a company that will make us rich. According to Warren Buffet, these super companies, ones with a durable competitive advantage come in three basic categories: they sell a unique product or service, or they are the low-cost buyer and seller of a product or service that the public consistently needs. The company that I have chosen to cover is Kraft Heinz, which is a company that sells a unique product and was recognized for it by Buffett himself. Kraft Heinz is a company that owns a piece of the customers' minds as they own multiple products that are popular amongst many households such as Heinz Ketchup, Kraft Mac and Cheese, Philadelphia Cream Cheese, etc. Because of Kraft Heinz’s ability to produce a unique product, it can sell its products at a higher price while still selling more of its products. Lastly, Buffet expresses the importance of durability for a company to have a successful competitive advantage, and Kraft Heinz has been producing some of the world’s most beloved products for 150 years.

I decided to pick Kraft Heinz as my company because I actively use many of their products such as their condiments, their mac-and-cheese, and their Jell-O. Also, I know Kraft Heinz has been able to establish itself as one of the most popular food-related brands, and wanted to research them and their financial information. What makes Kraft Heinz a good business is their commitment to continuously creating plans to grow as a business and continue its reign as one of the leading food and beverage companies in North America. Recently, at the 2023 CAGNY Conference, Heinz released their transformation momentum and path to lead the future of food. In this plan, Kraft Heinz provided several examples of how it would be renovating their iconic brands, delivering innovation, leading with disruptive marketing, and optimizing sales execution. According to Carlos Abrams-Rivera, the EVP and President, Kraft Heinz “plays at the intersection of food and technology, they see an opportunity for $2 billion in incremental net sales from innovation in North American retail from 2023-2027.” Kraft Heinz also expects Foodservice to be a global engine for growth in channels such as quick-service restaurants and school cafeterias. Lastly, Kraft Heinz has outlined growth opportunities it sees as it targets to grow net sales at a 13% compounded annual growth rate in the International zone.

Income Statement

When it comes to Kraft Heinz’s financials, there are a lot of numbers that contradict what Buffet believes a company with a durable competitive advantage should have. Revenue is always the first line on the income statement. This is the amount of money that comes in the door during the time in question. Just because a company is making a lot of revenue does not mean that it is earning a profit. The total revenue number by itself tells us nothing until we subtract the expenses and find out what the net earnings are. For the 2022 fiscal year, Kraft Heinz’s revenue was 26,485 million dollars. As you can see in the graph, this is the highest it has been since 2016, the year after The Kraft Food Groups and H.J. Heinz Co. merged. When it comes to the profit cycle, Kraft Heinz is currently at a normalized amount of profit, as over the past 7 years, they have continuously stuck around the 26,000 million dollar range.

Gross profit is how much money the company makes off of total revenue after subtracting the costs of the raw goods and the labor used to make the goods. Gross profit margin is the gross profit divided by original revenue. What creates a high gross profit margin is the company’s durable competitive advantage. Companies with gross profit margins of 40% or better tend to be companies with some sort of durable competitive advantage. As the gross profit margin continues to dip below 40% the company is experiencing fiercer competition. The gross profit margin for 2022 for Kraft Heinz was 30.66%. This indicates that Kraft Heinz is in a very competitive industry, which checks out as we know the food production industry is very congested with many different substitutes available. As you can see, over the last 9 years, Kraft Heinz’s profit margin has continuously been in the 30-35% range, but after hitting a peak in 2020 with a 35.05% GPM, Kraft Heinz is now on the decline when it comes to the profit cycle. According to Buffet, this means that Kraft Heinz is in a highly competitive industry, where competition is hurting overall profits.

Selling, General, and Administrative expenses are the costs for the direct and indirect selling and administrative expenses such as salaries, advertising, legal fees, etc. that occur during the accounting period. Companies that do not have a durable competitive advantage typically see a lot of competition and have a huge variation in SGA costs as a percentage of gross profit. When it comes to searching for a company with a durable competitive advantage, the lower the SGA expenses, the better. Typically anything under 30% of gross profit is considered good. Buffet believes that it is good practice to steer clear of companies with consistently high SGA costs. From 2016 to 2020, Kraft Heinz was hovering around the 38-39% range of SGA costs to gross profit but ever since 2021, it has risen to over 40% which shows that Kraft Heinz may be on the other side of a peak and entering a fall in the profit cycle.

Interest expense is the entry for the interest paid out, during the year, on the debt the company carries on its balance sheet as a liability. Interest is reflective of the total debt that the company is carrying on its books. Warren has figured out that a company with a durable competitive advantage often carries little or no interest expense. Warren’s favorite durable competitive advantage holders in the consumer products category all have interest payments of less than 15% of the operating income. According to Buffet’s description of a company with a durable competitive advantage in terms of percentage of interest expense to operating income, Kraft Heinz does not meet the criteria. While 2022’s interest expense was the lowest since 2014, Kraft Heinz is consistently spending 20% of its operating income on interest expenses. A decrease in interest expenses means we could be experiencing a contraction in our economy soon.

Income before tax is a company’s income after all expenses have been deducted, but before income tax has been subtracted. Warren uses this number when calculating the return he gets when buying a whole business or a partial interest in the company through shares. All investment returns, except for tax-free investments, are marketed on a pre-tax basis. Since all investments compete with each other, it is easier to think of them on equal terms. One of the cornerstones of Warren’s revelations is that a company with a durable competitive advantage is a kind of “equity bond.” After a massive loss in income in 2018, Kraft Heinz has done a decent job of recovering since then and is now close to 3,000 million in income before tax. While it isn’t yet the 2017 numbers they are on an increase which could potentially mean a contraction soon.

American corporations have to pay taxes on their income. What is interesting about Income Tax Paid is that the line item reflects the company’s true pre-tax earnings. Sometimes, companies like to tell the world that they are making more money than they are. Warren has learned that companies that are busy misleading the IRS are usually misleading their shareholders as well. If a company has a durable competitive advantage it is making so much money that it doesn’t have to mislead anyone. After looking at Kraft Heinz’s income taxes paid since 2014, the tax rate on their income has fluctuated each year, which is something that Warren is not looking for in a company.

After all the expenses and taxes have been deducted, we get the company’s net earnings.

When looking for a company with a durable competitive advantage, Warren looks for a company’s net earnings to have a historical upward trend. While the ride doesn’t need to be smooth, the overall historical trend has to be upward. While a lot of financial analysis focuses on a company’s per-share earnings, Buffet is more focused on the business’s net earnings to see what is going on. A company with a durable competitive advantage will also report a higher percentage of net earnings to total revenue than its competitors will. If a company is showing a net earnings history of more than 20% of total revenues, then there is a high chance it is benefiting from a durable competitive advantage. Looking at Kraft Heinz's net earnings numbers, they are not good compared to what Buffet looks for in a company with a durable competitive advantage, while they are on an upward trend from 2014 to 2022, the percentage of net earnings to total revenue is nowhere near the 20% that Buffet like to see. Based on these numbers, I would expect Kraft nearing a peak in the profit cycle.

Per-share earnings are the net earnings of the company on a per-share basis for the time in question. The more a company earns per share, the higher the stock price. A per-share earnings figure for ten years can give us a very clear picture of whether the company has a long-term advantage. Warren looks for consistency and an upward trend. Consistent earnings are usually a sign that the company is selling a product that doesn’t need much change. An upward trend is usually a sign that the company is strong enough to increase its market share or use financial engineering. While there has been a slight upward trend from 2014 to 2022 in Kraft Heinz’s per-share earnings, there has been little to no consistency which goes against Buffet’s idea of a company with a durable competitive advantage.

Many of the numbers in Kraft Heinz’s income statement are not promising when it comes to what Buffet looks for in a company with a durable competitive advantage. Since 2014, there has been little to no consistency in almost every data point mentioned, which is not something an investor who wants to get rich would want to see in a company.

Balance Sheet

Assets are where the goods are kept, things such as cash, plant and equipment, patents, and all the stuff the riches are made of. Current assets are made up of cash or assets that can be converted into cash in a very short time. Assets are listed on the balance sheet in order of their liquidity. A company’s assets help Warren determine whether or not the company has a durable competitive advantage. Total assets are important in determining just how efficiently a company is putting its assets to use. A company’s efficiency can be measured by its return on asset ratio. A really high return on assets, though, may indicate vulnerability in the durability of the company’s competitive advantage. Since 2015, Heinz Kraft has been on a consistent decline in the amount of total assets they have on their balance sheet, and their return on asset ratio has been very low.

A high number for cash or cash equivalents tells Warren that the company has a competitive advantage that is generating tons of cash, or it just sold a business or a ton of bonds, which may not be a good thing. A low amount of cash generally means the company has poor economics. If a company has a lot of cash and little debt, it will probably make it through tough times, but if a company has little cash and a lot of debt, it is probably a sinking ship that can’t be saved. Buffet says to look at a company’s cash over the past seven years to see if they are consistently bringing in more cash. This would indicate that the company has a durable competitive advantage. As we can see, Kraft Heinz's cash has fluctuated ever since 2014 which is not what Warren is looking for.

Inventory is the company’s products that it has warehoused to sell to its vendors.

Manufacturing companies with a durable competitive advantage have an advantage, in that the products they sell never change and therefore never become obsolete, which is something Warren wants to see. It is important to look for companies with inventory and net earnings on a corresponding rise and not companies that see jumps and falls in inventory numbers. As we can see with Kraft Heinz’s inventory numbers they are on a consistent rise for the most part, however, they are not on a corresponding rise with net earnings.

Net receivables are the money that is owed to the company. Net receivables tell us very little about a firm and its competitive advantage, but if a company consistently has a lower percentage of Net Receivables to Gross Sales than its competitors, it usually has an advantage working in its favor. In 2016, Kraft Heinz was able to get to a low percentage of net receivables to gross sales of 8.41%, but since then Kraft Heinz has seen an increase reaching up to 26.10% in 2022, which is something Buffet does not want to see.

Companies that do not have a long-term competitive advantage are faced with constant competition forcing them to continuously get new equipment, which creates more expenses. A company with a competitive advantage will be able to finance any new plants and equipment internally. Producing a consistent profit that doesn’t have to change leads to consistent profits. Since 2018, Heinz Kraft has seen a consistent decline in their property, plant, and equipment. This is a good thing as that means they do not have to constantly buy new equipment and they can rely on their brand name of Heinz and Kraft to have consumers continue to buy their products.

Short-term debt is money that is owed by the corporation and due within the year.

Aggressively pursuing short-term debt can hurt a company. Protecting a durable competitive advantage is a lot easier than getting it back. For the most part, Kraft Heinz has done a great job of keeping their short-term debt low, which is something Buffet is looking for in a company.

Long-term debt is debt that matures any time past a year. Companies that carry a long-term competitive advantage often carry little or no long-term debt on the balance sheet.

Companies that have enough earning power to pay off their long-term debt in under three or four years are good candidates for a durable competitive advantage. Leveraged buyouts can sometimes occur which can create debt, but it is good to remember that little long-term debt often means a good long-term bet. While over the past 2 years, Kraft Heinz has seen a significant drop off in their amount of long-term debt, their debt numbers are still too high for a company that Buffet would buy.

Total liabilities is the sum of all liabilities of the company. Total liabilities are important in helping us determine debt to shareholder’s equity which can give us a good idea of whether or not a company has a durable competitive advantage. Debt to shareholder’s equity typically tells us whether or not a company is using debt to finance its operations or equity. A company with a durable competitive advantage should show a higher level of shareholder’s equity, a lower level of liabilities, and therefore a low debt-to-equity ratio. Any time we see a company with a debt-to-equity ratio of .80 or lower, there is a very good chance we are looking at a company with a durable competitive advantage. As you can see, the Debt-To-Equity ratio of a kraft Heinz continuously hovers around 1.0 which according to Buffet is not a great sign as he would like to see a ratio of .80 consistently.

Shareholder’s equity, or book value, is the net worth of the company after subtracting all of the liabilities from all of the assets. This is the amount of money that the company’s owners/shareholders have initially put in and have left in the business to keep it running. Shareholders equity allows us to calculate the return on shareholder’s equity, which gives us a good idea of a company with a durable competitive advantage. In 2017, Kraft Heinz’s shareholders’ equity hit a peak that they quite haven’t been able to reach since then, but since 2018, their shareholders' equity has remained relatively steady with a slight decline.

Common stock represents ownership in a company. Preferred stocks, while they don’t have voting rights in the company that common stockholders do, do have a right to a fixed dividend that must be paid before the common stock dividend. Preferred and common stocks are carried on the books at their par value. Any money over par that was paid when the company sold the stock is carried on the books as “paid in capital”. Companies that have a durable competitive advantage tend not to have preferred stocks. In this sense, Kraft Heinz is a company that has a durable competitive advantage because they do not have preferred stock on their balance sheet.

Retained earnings are earnings from a company that is retained to keep the business growing. Retained earnings, if profitably put to use, can greatly improve the long-term economic picture of the business. Retained earnings are a cumulative number. A continuously growing retained earnings number for a company is a good indicator of whether the company has a durable competitive advantage. White Kraft Heinz was in the negatives for retained earnings from 2018 to 2021, it found its way out and back into the positives through continuous growth which is a promising sign for Buffet and his beliefs.

Treasury stock is stock that had been bought back by the company and held on to with the intent to reissue at a later date. While treasury stocks are arguably looked at as an asset, they are carried on the balance sheet as a negative value because they represent a reduction in the shareholder’s equity. One of the hallmarks of a company with a durable competitive advantage is the presence of treasury stocks on the balance sheet. Not only does Kraft Heinz have treasury stock on their balance sheet but it has consistently gone up every year which is good for what Warren looks for in a company with a durable competitive advantage.

Financial analysts have developed the return on shareholder’s equity equation to test management’s efficiency in allocating the shareholder’s money. Return on shareholder’s equity can be calculated by dividing net earnings by shareholder’s equity. A company with a durable competitive advantage has a higher-than-average return on shareholder’s equity. As time goes on, high returns on equity will add up and increase the underlying value of the business. Outside of one year, Kraft Heinz has had a positive return on shareholder’s equity, however, it has not been higher-than-average, which is something that Buffet is looking for. This could be because Kraft Heinz is in the highly competitive grocery market.

Financial Analysis

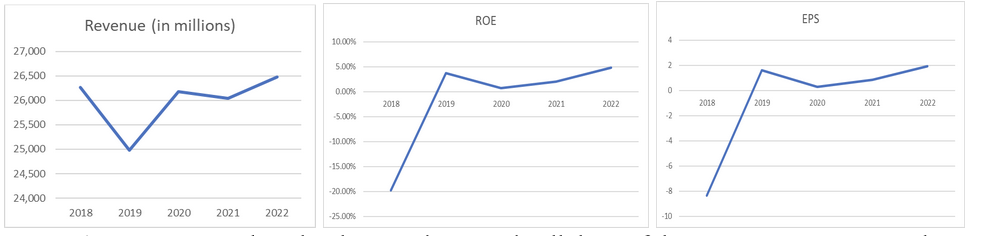

Below is the 5-year time series graph on revenue, ROE, and EPS for Kraft Heinz:

As you can see, there has been an increase in all three of these measurements over the past five years. Throughout this time, Kraft Heinz’s growth rate in sales was 0.83%, going from $26,268 in 2018 to $26,485 in 2022. Kraft Heinz’s ROE has increased from as low as 20% up to 5%. Lastly, the growth rate in EPS was 21.38%, going from 1.59 in 2019 to 1.93 in 2022. I did not include 2018 in the calculation of the growth rate for EPS because 2018 was an outlier of -8.36 EPS. All of these increases are positive signs for investors looking at whether to invest in Kraft Heinz.

Measured by the S&P 500 index, the average stock market return is about 10% and has been for nearly the past century. According to the Kraft Heinz 10K for 2023, Kraft Heinz pays out $0.40 per share of common stock. Lastly, the one-year target estimate of Kraft Heinz stock, according to Yahoo Finance, is $36.45. With all of this in mind, my estimate of the intrinsic dollar value of the entire business is $33.5.

Using the Dividend Discount Model, my fair value of Kraft Heinz would be $36.82. Price-to-sales for Kraft Heinz is $1.50. Price-to-earnings is $11.19. Price-to-book value is $0.83. Using the multiples approach, Kraft Heinz’s price-to-sales ratio is lower than PepsiCo and General Mills, but higher than Tyson Foods. Kraft Heinz has the lowest forward price-to-earnings ratio as well as the lowest price-to-book ratio.

After assessing Kraft Heinz and comparing it with other companies as well, I do not believe that there is a price-to-value gap. My intrinsic value estimate of $33.50 per share is only about 40 cents higher than what the company is currently selling for on the stock market and compared to its competitors Kraft Heinz is not doing as well when it comes to their ratios.

Overall Assessment

Based on what Buffet believes to be the factors of a company with a durable competitive advantage, Kraft Heinz’s financial statements did not showcase a lot of those factors, and in some cases showed the complete opposite. With that being said, Kraft Heinz’s sustainable competitive advantage is that they sell a unique product and have a very strong and memorable brand name for a lot of their products.

Now while Kraft Heinz does have a strong and memorable brand, there are many competitors that they face in the food and beverage industry. According to Statista, Kraft Heinz was the fifth-largest food and beverage company in North America in 2021-2022. The companies that were in front of Kraft Heinz were PepsiCo, Tyson Foods, JBS USA, and Nestle. Some brands underneath Kraft Heinz were Coca-Cola, General Mills, and Mars. Kraft Heinz also faces many different threats to their company as well. One of the biggest barriers to entry for the food and beverage industry is the highly competitive nature. The food and beverage industry has been around forever, which means there are thousands of companies trying to compete for the market share of the industry. Another barrier is the threat of substitution. The threat of substitution is high in food and beverage companies since many companies are offering very similar products.

According to Kraft Heinz’s 10K for 2023, their top three drivers of earnings for the 2022 fiscal year were condiments and sauces, cheese and dairy, and ambient foods. In millions, condiments and sauces produced $8,241, cheese and dairy produced $3,976 and ambient foods produced $3,047. These 3 main drivers are encouraging to see as they are products that many households typically consume in their everyday lives.

Looking back at Kraft Heinz’s financials, it is safe to say that they have financial leverage. This is because they have high total liabilities numbers and have a relatively high debt-to-equity ratio compared to what Buffet would like to see in a company. Similarly, Kraft Heinz is not a capital-intensive company as in 2022, only about 7 percent of their total assets came from plant, property, and equipment.

Now the predicament comes of whether or not I would buy or sell Kraft Heinz stock today. I think Kraft Heinz’s stock is a very interesting one to look at and determine how it should be used. While many of Kraft Heinz’s numbers on both their income statement and balance sheet don’t indicate that they are a company with a durable competitive advantage, I still believe that their name brand carries a lot of weight and allows them to be a successful company to invest in at certain points in the macroeconomy. As I have mentioned throughout this paper, Kraft Heinz is in the food and beverage industry, which is highly competitive. With that being said, they are also a defensive industry which means their stock price is not very sensitive to the business cycle. Because of this, I think at this point, I would sell shares of Kraft Heinz today. I do however believe that we could be seeing a peak in the economy come a time soon and right as the economy begins to take a hit I would buy Kraft Heinz’s stock since it is a defensive industry, and a very successful one for that matter. In the 5-year time series graph of ROE for Kraft Heinz, there was a slight dip in the ROE from 2019 to 2020, which as we know was the year the COVID-19 pandemic first began. After this though, Kraft Heinz was able to recover and see an increase in their ROE. If there is a contraction in the economy coming soon, as I believe there is, I would wait for the contraction to occur before I invest in the company.